*While I am a licensed Realtor®, I am not acting as your Realtor. Every real estate situation is unique, so please consult a professional who can provide advice tailored to your needs.*

If you have been hearing rumblings about 50-year mortgages, you are probably wondering if this is actually happening or if TikTok is just bored again. Before we decide whether a 50-year mortgage is smart or scary, it helps to zoom out and understand how the current system was built and how interest rates historically behaved.

Here is a breakdown of how we got the 30-year mortgage and what a 50-year version could mean for homeowners.

A Quick History of Mortgage Evolution

Before the 1930s

Mortgages were:

- Three to five-year terms

- Interest only payments

- Huge balloon payment at the end

- High default risk

- Designed to protect banks, not borrowers

Homeownership was not realistic for most households.

The Great Depression Hits (1929)

Everything fell apart all at once.

- Banks collapsed

- Refinancing became impossible

- Nearly half of all mortgages defaulted

- The housing market froze

This collapse forced the government to redesign the mortgage system.

1933 to 1938: The Full Rebuild

Key milestones:

- 1933: HOLC refinances borrowers into longer, fully amortized loans

- 1934: FHA is created and introduces fixed rate, amortized mortgages with lower down payments

- 1938: Fannie Mae is established and brings liquidity and standardized underwriting

These changes made mortgages safer, longer, and more accessible.

When the 30-Year Mortgage Took Over

- Introduced by the FHA in 1934

- Became the widely adopted standard in the 1950s

- Lower payments made homeownership possible for millions

- Predictable payment structure built long term stability

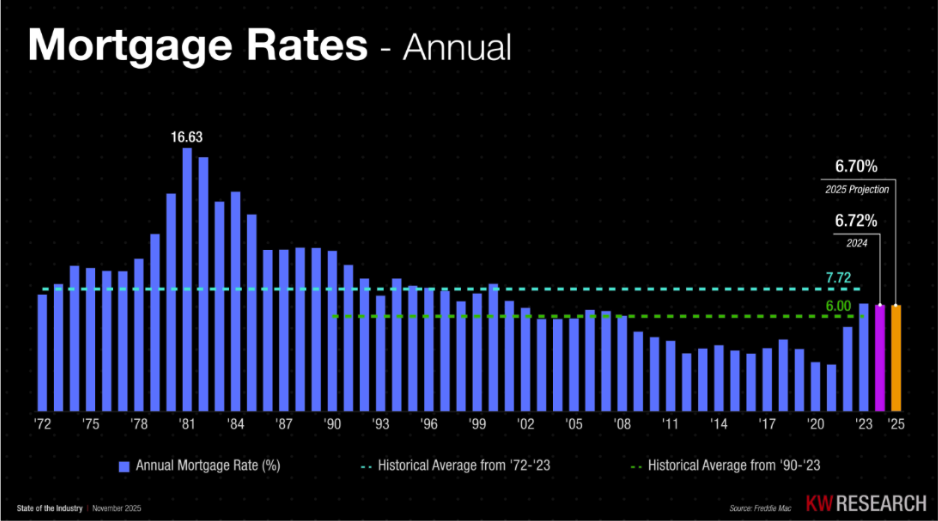

Interest Rates Over Time

Let’s talk about rates. Today, buyers are hesitating to take on a rate in the 6% range, but 6% is historically a really decent rate. We just have short memories and remember when rates were less than 4% during the pandemic era, but that’s likely not coming back anytime soon.

Here are some interesting takeaways:

- The historical average mortgage rate from 1972 to 2023 is 7.72%

- The historical average mortgage rate from 1990 to 2023 is 6%

- That means many of today’s buyers are comparing current rates to the pandemic era unicorn years rather than the true long term normal

If you’d like to check where rates are today, take a look at MortgageNewsDaily.Com.

Visual recap of the chart

- Rates peaked in the early 80s at 16 to 18% which seem unfathomable, but people were still buying real estate.

- Rates trended down from the 90s through 2021

- The 2020 to 2021 lows were an anomaly and they were great while they lasted, but it’s unlikely we’re going to see rates that low again…and if we do, we probably have bigger fish to fry.

- Current rates sit right in line with historical norms, so if prices are down, it could be the right time for you to jump into the market!

This context matters when evaluating conversations around affordability and loan terms.

The 50-Year Mortgage Conversation

The idea is simple. Stretch out the repayment timeline to lower the monthly payment. But the math tells a different story.

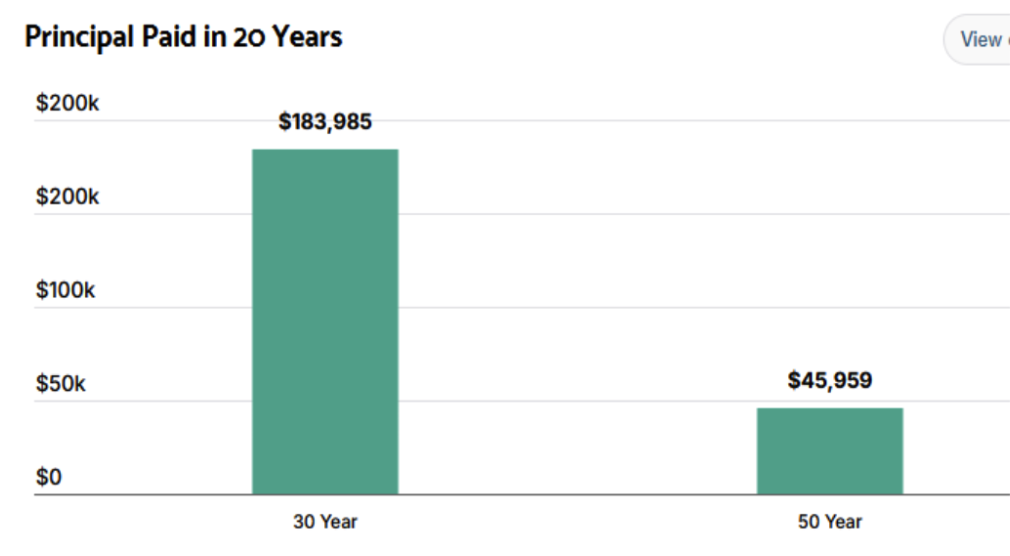

Chart comparison you provided: Principal Paid in 20 Years

- 30-year mortgage: You pay down about 183,985 dollars of principal

- 50-year mortgage: You pay down about 45,959 dollars of principal

That is a massive difference in equity and long term wealth

What a 50-year mortgage would actually mean

Pros:

- Lower monthly payment

- Higher approval odds

- Could help first time buyers enter the market

Cons:

- Very slow equity growth

- Far higher total interest paid

- Homeowners stay debt tied for most of their adult life

- Wealth building becomes dramatically slower

Other countries like Japan have experimented with ultra long mortgages, but the United States has rarely changed mortgage structure unless the entire system is failing.

Right now, the 50-year conversation feels more like a symptom of affordability pressure than an actual policy shift coming down the pipeline.

What Buyers Need To Know

- The 30-year mortgage exists because it balances manageable payments with healthy equity growth

- Historically, rates in the 6 to 7% range are normal

- A 50-year mortgage would reduce payments but slow down wealth building

- Until policymakers decide the system is broken enough to overhaul again, the 30-year mortgage is here to stay

T. Kerr Property Group is proud to be voted top Realtors in Round Rock and Georgetown. They’ve won accolades including: PT50, ABJ Residential Real Estate Award, and have been featured in Real Producers. Most importantly, the T. Kerr Property Group gives back to their community and are recognized experts across Georgetown, Round Rock, Austin, and surrounding areas. Whether you’re buying, selling, or investing, T. Kerr Property Group is here to help you make informed, confident real estate decisions.