*While I am a licensed Realtor®, I am not acting as your Realtor. Every real estate situation is unique, so please consult a professional who can provide advice tailored to your needs.*

If you’ve recently come into money – maybe from selling a property, receiving a bonus, an inheritance, or even winning the lottery – you may be sitting on a financial opportunity most homeowners overlook. That extra cash can do more than just sit in your bank account or get eaten up by inflation. Used strategically, it can help you slash your monthly payments, cut years off your loan, and save hundreds of thousands in interest through recasting or refinancing your mortgage.

Let’s unpack what each of these options means, when to use them, and how much you could actually save.

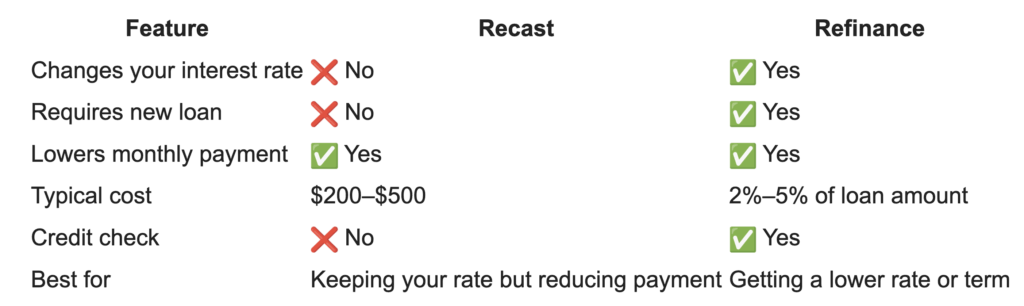

What Is a Mortgage Recast?

A mortgage recast (sometimes called a loan re-amortization) allows you to apply a large lump-sum payment toward your existing mortgage principal and then have your lender recalculate your monthly payments based on that lower balance.

Unlike refinancing, you keep your existing loan and interest rate – the only thing that changes is your payment amount and how much you’ll save over time.

Key Benefits of Recasting:

- Lower monthly payments without changing your rate or term

- Minimal paperwork – often just a small lender fee

- No new credit check or appraisal

- Great for homeowners who like their current rate but want smaller payments

Considerations:

- Not all loans are eligible (check with your lender)

- You must have a lump sum available (usually at least $5,000–$10,000)

- Does not shorten your loan term unless you keep paying your old amount

What Is a Mortgage Refinance?

A refinance replaces your current loan with a new one – often at a lower interest rate or different term. When mortgage rates drop, this can be one of the most powerful financial moves homeowners make.

Key Benefits of Refinancing:

- Can significantly reduce your interest rate and payment

- Opportunity to shorten your loan term (for example, 30 years to 15)

- May allow you to tap into equity for home improvements or investments

Considerations:

- Closing costs usually range from 2%–5% of the loan

- Requires a new appraisal and credit approval

- If rates aren’t much lower, savings may take years to recoup

Recast vs. Refinance — Quick Comparison

Real-World Example: $500,000 Mortgage

Let’s look at a 30-year loan at 7% interest.

- Original Loan Payment: $3,326/month

- Total Interest Over 30 Years: $697,544

Now let’s see what happens with two smart strategies:

| Scenario | Monthly Payment | Total Interest | Interest Saved |

|---|---|---|---|

| Original Loan (7%) | $3,326 | $697,544 | — |

| Recast with $100K Lump Sum | $2,661 | $558,036 | $139,500 |

| Refinance at 5% | $2,684 | $466,279 | $231,000 |

(Source: Sample calculation using amortization formula; rates approximate as of 2025. Data cross-referenced with Freddie Mac and Realtor.com average mortgage rate trends.)

The Power of Recasting and Refinancing – By the Numbers

Over the life of a 30-year loan, the savings potential is staggering:

- Recasting your existing 7% loan with $100,000 can save nearly $140,000 in interest.

- Refinancing to a 5% loan can save more than $231,000 – and that’s after accounting for closing costs in many cases.

In other words, the right choice today could mean freeing up hundreds of thousands of dollars for your future, your family, or your next investment. Whether you’re planning to stay long-term or simply want to strengthen your financial position, these two tools are among the smartest moves in homeownership.

Which Option Is Right for You?

If you’re sitting on cash and your rate is already competitive, recasting might make the most sense. You’ll lower your monthly payments without the hassle of a full refinance.

But if interest rates drop or your credit profile has improved since you bought your home, refinancing could dramatically reduce your long-term costs – even if your payment only drops a few hundred dollars.

Before making a move, talk with a local real estate expert or mortgage professional who understands how both options align with your personal goals and current market trends.

Final Thoughts

In today’s evolving real estate landscape, it’s not just about buying or selling – it’s about managing your money wisely once you own. Recasting and refinancing are two underused strategies that can help homeowners in the Austin and Georgetown areas build long-term wealth faster.

If you’re ready to explore your options, reach out to our team – we’ll help you evaluate the numbers and make the choice that best fits your future.

T. Kerr Property Group is known for an unwavering commitment to excellence in Central Texas real estate, earning a reputation as one of the top Realtor teams in the region. The team has received numerous industry honors, including recognition from PT50 and the ABJ Residential Real Estate Awards. What matters most, however, are the awards voted on by the community, such as Best Realtors in Round Rock and Best of Georgetown. T. Kerr Property Group is the trusted choice for buyers and sellers in Austin, Georgetown, Round Rock, and the surrounding areas, consistently recognized for outstanding performance and exceptional client care.